Pehlivankoy Natural Gas Discovery, Thrace Basin, Turkey

Block F17-b4

Gazelle is the operator with a 100% working interest in the F17-b4 Petroleum License in the Thrace Basin of Western Turkiye. The petroleum license was awarded on January 26, 2019 and comprises 145 square kilometers.

Gazelle is the operator with a 100% working interest in the F17-b4 Petroleum License in the Thrace Basin of Western Turkiye. The petroleum license was awarded on January 26, 2019 and comprises 145 square kilometers.

The legacy well, Pehlivanjkoy-1 was drilled by TPAO in 1992, and encountered a working petroleum system and tested natural gas at non-commercial rates from stacked reservoirs. The main tight gas reservoirs are the Teslimkoy-1 (T-1) and Teslimkoy-2 (T-2) reservoirs within the Mezardere formation, which have 25 m and 16 m of gas pay, respectively. Several other intervals also tested natural gas at low rates. The prevailing drilling and completion techniques employed at the time are now deemed to have been sub-optimal for the development of these tight gas sands.

Sections

Pehlivanköy-1

The license contains the Pehlivanköy natural gas discovery, originally drilled in 1992 has been reevaluated and assigned 27 Bcf of 1P, 65 Bcf of 2P and 376 Bcf of 3P reserves in a market with robust gas pricing.

Pehlivanköy-2

Pehlivanköy-2 was spudded on June 6th, 2023, and drilled in 28 days to a depth of 3,045m (MD). The initial well results of the reservoirs discovered in the offsetting P-1 well are very encouraging. In addition to the two targeted Teslimköy zones discovered in P-1, three other prospective gas intervals were encountered during drilling. Management estimates are of a total of 50 meters of net pay across the various zones.

The Company designed a multi-zone completion and testing program, based on the evaluation of the core and open-hole logs that were acquired by Weatherford. This program commenced in March 2025.

Both primary target reservoirs, Teslimköy-1 (“T-1”) and Teslimköy-2 (“T-2”), were hydraulically fracture-stimulated by Schlumberger. All indications were consistent with the frac jobs being pumped successfully, and almost exactly as modelled. Both Teslimköy reservoirs were allowed to flow back for several days, resulting in recovery of approximately 50% of load fluid. Continuous slugging of gas along with frac fluid was observed at surface throughout the flow-back period.

Two additional uphole gas reservoirs, the Upper Mezardere-1 (UM-1) and the Upper Mezardere-2 (UM-2) were perforated on wireline before running the final completion, which was designed to allow for selective testing of the four individual reservoirs.

A 10-day workover operation of the Pehlivanköy-2 well was completed in late August 2025. Coiled-tubing was used to lift the well with nitrogen, allowing flow rates to be measured from each of the primary Teslimköy-1 and Teslimköy-2 reservoirs that were hydraulically stimulated in May 2025. Flow rates achieved from Teslimköy-1 exceeded 375 Mcf/day and from Teslimköy-2 exceeded 150 Mcf/day, but were not able to be stabilized under the existing completion conditions. Gazelle estimates that each zone could produce between 500 and 2000 Mcf/day in a production scenario. Gazelle intends to return to Pehlivanköy-2 in Q2 2026 for an extended, long-term flow test to establish commercial flow rates for these reservoirs.

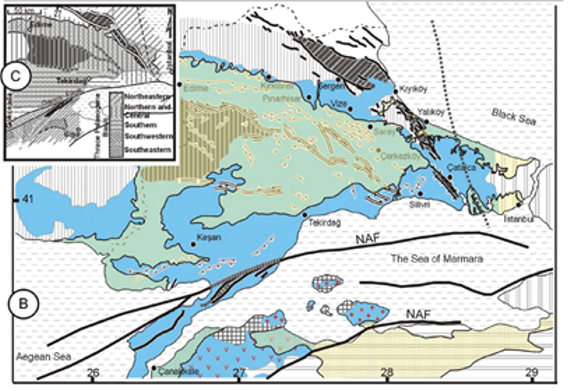

Thrace Basin Geology

The Thrace Basin is predominantly a gas basin, comprising up to 9000m of Eocene to Miocene marine and terrestrial clastic sediment. The basin formed in response to dextral strike-slip motion along the North Anatolian Fault system, which forms its southern boundary. Initial deposition occurred during the final stages of Palaeogene transtension. Post late Oligocene, the basin continued to evolve in an intermontane compressional tectonic setting. Cenozoic basin fill divided by a middle to late Miocene unconformity, was deposited in a variety of environments. Deep-water marine, pro-delta and fluvial shales provide the source material. Reservoirs are found in turbidite basin-floor fans and channels, deltaic and fluvial sandstones. The Cenozoic sedimentary package overlies Paleozoic to Mesozoic metamorphic basement.

Tectonic setting of the Thrace Basin (Elmas, 2011).

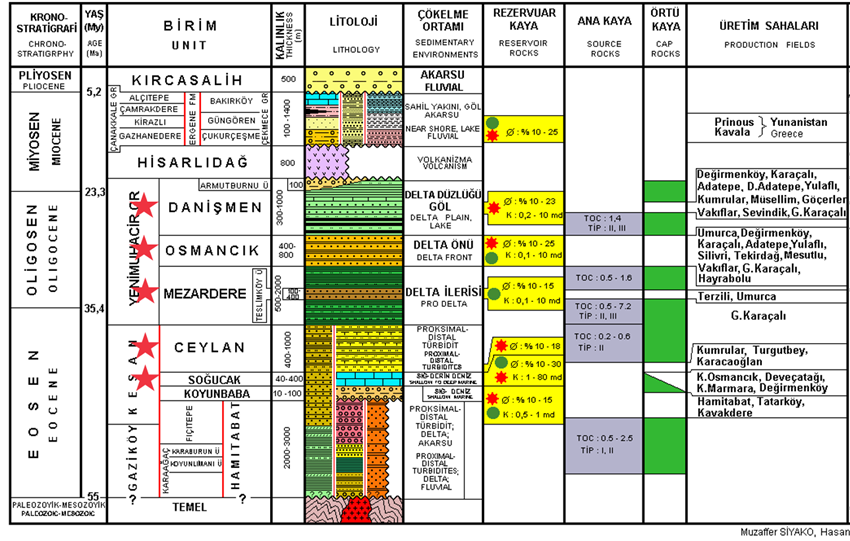

Stratigraphy and Petroleum System Elements of the Thrace Basin (After Siyako & Huvaz, 2007).

Pehlivanköy Gas Discovery

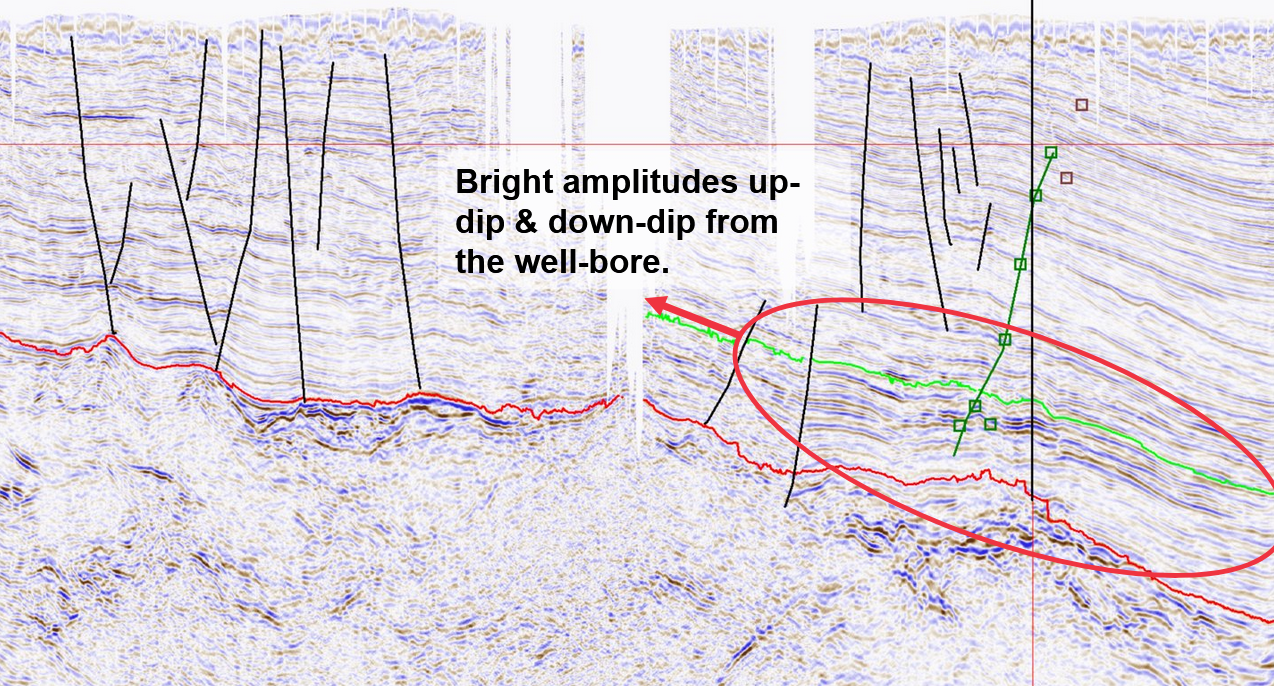

In late 2019, Gazelle acquired 325 square kilometers of existing raw 3D seismic data, covering ~90% of the F17-b4 Petroleum License. The seismic data was determined to be of excellent quality and was processed in Calgary. The interpretation of the data revealed seismic amplitude anomalies tied to the gas reservoirs encountered in the Pehlivankoy-1 and Pehlivakoy-2 wells. Additional seismic amplitude anomalies were encountered on other portions of the license without well penetrations. Gazelle has developed a drillable prospect inventory with potentially meaningful upside, comprising multiple exploration plays, both conventional and unconventional.

The amplitude signature associated with the conventional sand reservoirs discovered by Pehlivanköy-1 is readily discernible. In December 2022, our reserve auditor, Degolyer & MacNaughton (D&M), assessed the volume of gas associated with the discovery as 27 Bcf GIP at 1P level of confidence, 65 at 2P, 376 Bcf at a 3P.

The opportunity offers low-risk and low-cost access to a material resource base in a stable political and fiscal environment with large upside potential.

On December 9, 2025 the exploration license was extended for two years (until January 2028) by the Turkish petroleum regulator, MAPEG. This extension included the carry forward of the second commitment appraisal well from the initial five-year exploration period. In case of discovery, a production lease is granted for 20 years, which may be extended twice for periods not exceeding 10 years at a time.

Figures showing cross-section through Pehlivanköy-1 wellbore as well as a total area of 25 m sand alone = 2123 ha (21.23 sq km) within the development area.

Fiscal Regime and Market

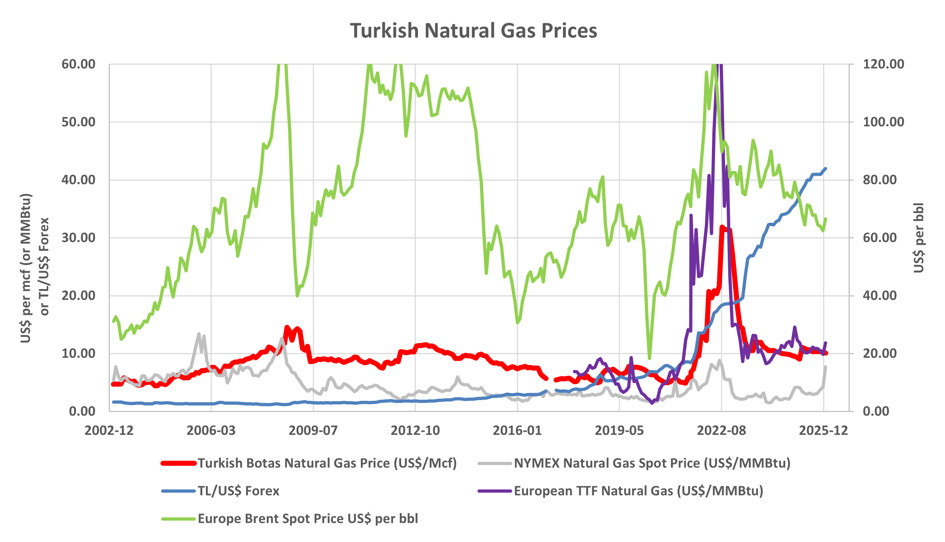

Turkish gas prices and fiscal terms are excellent, and globally competitive. Turkey itself produces about 2% of its own natural gas consumption – a local market. Additionally, the F17-b4 block has several potential tie-in points to the Turkish domestic grid that are 13 to 24 km from the Pehlivankoy field and about 40 to 60 km from the export pipelines to Europe.

- January 2026 Gas Price = US $10.11/Mcf

- Royalty = 12.5%

- Corporate Tax Rate = 25%

Gas Pricing

Gas price in Turkish Lira is adjusted regularly to track price of imported gas, primarily from Russia, and offset devaluation of the Turkish Lira.

BOTAS, the state-owned pipelines and trading company in Turkey currently controls approximately 80% share of Turkey’s natural gas imports, and is expected to be the main potential purchasers of any new domestic natural gas production. BOTAS' pricing structure effectively sets the domestic market due to its dominant position.

Development Program

Drilling : Drilling will be performed in two phases. Phase 1 will consist of two appraisal wells. Phase 2 will be designed and executed based on the analysis of geological data obtained from the Phase 1 and subsequent wells. Phase 2 will consist of 7 to 90 wells for the Reserve scenarios (1P, 2P, and 3P). A separate drilling program will be planned to explore the prospective resources.

Production: The produced gas will be sold through the national grid, and the condensate will be sold locally. The production will be managed with objectives of output optimization and cost control, with all parameters continuously benchmarked against those of other companies operating in the area.

Infrastructure: The Thrace Basin is well-served with natural gas pipelines. A natural gas processing plant will be built for separation of condensate and dehydration of the gas. There are several tie-in options including the regional gas distribution network.